Short-Selling Restrictions During COVID-19

Financial regulators restricted short selling in March 2020 after global stock markets declined in response to the COVID-19 pandemic (Otani 2020). As market participants grappled with uncertainty about quarantine measures, travel restrictions, and other impediments to commercial activity, authorities identified short-selling as a potential threat to market stability. By limiting the trading strategy, authorities attempted to keep financial markets fair, orderly, and efficient. Though scholars argue that short-selling restrictions can exacerbate market turbulence, policymakers banned short-selling for several months in a row.

An investor conducts a “short sale” by borrowing a security, then selling it to another party. If the security’s price later drops below the original sale price, the investor repurchases the security at the lower price, returns the security to the original lender, and profits on the difference in prices; if the price rises, the short-seller may take a loss. In a so-called “naked” short sale, the investor agrees to sell a security to a third party without first obtaining the security. A short sale becomes “covered” once the investor repurchases the security so that it may be returned to the original lender. Regulators have restricted both kinds of short selling at various scopes: for entire securities exchanges, specific security, or sectors. Other restrictions include short-selling volume limits and “uptick” rules, which require investors to wait until a given security’s price rises before they are allowed to short-sell it.

Regulators implementing short-selling restrictions or bans in the wake of the COVID-19 pandemic primarily structured the policies to expire after a few months and largely banned short sales on entire exchanges. Others that did not prohibit short selling altogether approved measures that attempt to limit the practice or curb harms they associated with short sales. European regulators tended toward broader bans, while various Asian policymakers tweaked financial market rules to restrict short selling.

During the Global Financial Crisis (GFC), policymakers implemented various short-selling restrictions (SSRs). Regulators in various countries, including Denmark, Switzerland, and the U.S., banned short selling of shares in certain financial institutions that were later lifted (Beber and Pagano 2013). Japan’s Financial Services Agency banned naked short selling in October 2008, extended the ban 12 times, then made the ban permanent five years later (Osaki 2013; Financial Services Agency 2014).

One decade later, regulators pursued similar SSRs, captured in Table 1. Authorities said they were restricting short selling to preserve market confidence and financial stability, which were threatened by the rapid onset of the COVID-19 outbreak: market participants had little time to absorb information about the virus and public health interventions, evaluate securities based on the information, or trade according to those valuations. As global prices plunged and volatility spiked, authorities said they hoped to prevent traders from trading on imperfect information, betting on market turmoil, and threatening the viability of the underlying companies.

However, research has consistently shown that banning short selling during stretches of particularly volatile equity market activity intensifies the volatility. Such prohibitions impede investors from determining accurate prices of assets and reduce market liquidity. Moreover, short-selling bans in one market can increase volatility in other markets as some investors try to circumvent the ban.

Table 1

|

Country |

Enactment Dates |

Policy Type |

|

Austria |

March 18 to May 18, 2020 |

Index/Exchange-Wide Ban |

|

Belgium |

March 17, 2020 Trading Day |

Securities-Targeted Ban |

|

Belgium |

March 18 to May 18, 2020 |

Index/Exchange-Wide Ban |

|

European Union |

March 16, 2020 to March 19, 2021 |

Heightened Transparency Measure |

|

France |

March 17, 2020 Trading Day |

Securities-Targeted Ban |

|

France |

March 18 to May 18, 2020 |

Index/Exchange-Wide Ban |

|

Greece |

March 18 to May 18, 2020 |

Index/Exchange-Wide Ban |

|

India |

March 23 to October 29, 2020 |

Derivative Short Position Limits |

|

Indonesia |

March 2, 2020 to Further Notice |

Index/Exchange-Wide Ban |

|

Italy |

March 13, 2020 Trading Day |

Securities-Targeted Ban |

|

Italy |

March 17, 2020 Trading Day |

Securities-Targeted Ban |

|

Italy |

March 17 to May 18, 2020 |

Index/Exchange-Wide Ban |

|

Malaysia |

March 24 to December 31, 2020 |

Index/Exchange-Wide Ban |

|

Pakistan |

April 1 to April 30, 2020 |

Uptick Rule |

|

South Africa |

March 12 to Present |

Settlement Procedure Changes |

|

South Korea |

March 10 to March 13, 2020 |

Lowered Threshold that Prompts Stock-Specific Short-Selling Ban |

|

South Korea |

March 13 to March 15, 2021 |

Index/Exchange-Wide Ban |

|

Spain |

March 13, 2020 Trading Day |

Securities-Targeted Ban |

|

Spain |

March 17 to May 18, 2020 |

Index/Exchange-Wide Ban |

|

Taiwan |

March 19 to June 10, 2020 |

Uptick Rule |

|

Taiwan |

March 19 to June 10, 2020 |

Limited Short-Selling Volumes |

|

Thailand |

March 13 to September 30, 2020 |

Uptick Rule |

|

Turkey |

February 28 to Further Notice |

Index/Exchange-Wide Ban* |

|

Turkey |

July 6, 2020 to Further Notice |

Banned 6 Banks from Short Selling |

|

United Arab Emirates |

March 9 to Further Notice |

Index/Exchange-Wide Ban |

|

United Kingdom |

March 13, 2020 Trading Day |

Securities-Targeted Ban |

|

United Kingdom |

March 17, 2020 Trading Day |

Securities-Targeted Ban |

*Turkey’s regulators lifted the ban for Borsa Istanbul’s top 30 stocks on June 30.

As Table 1 shows, regulators have included various features in short-selling restriction policies. Their key design decisions include:

- Administration

- Coordination

- Justification

- Restriction Type

- Scope

- Timing and Duration

- Related Short-Selling Rules.

Administration

SSRs are typically enacted by a financial regulator, such as a securities commission, and an exchange. Exchanges are typically private organizations and are considered “self-regulatory organizations” in the U.S. and other countries. During the COVID-19 crisis, some regulators issued new SSRs to exchanges, others approved SSRs proposed by exchanges, and several jointly declared SSRs alongside their exchanges. For the European Union, the European Securities and Markets Authority (ESMA) is an overarching financial regulator that works with member states’ national authorities to construct and coordinate the restrictions.

Coordination

Coordination minimizes the risk of regulatory arbitrage that could arise from the nonuniform application of SSRs. Securities representing the same company often trade on several exchanges across several countries at once. The targets of one country’s SSR, including multinational financial products and indexes, sometimes represent securities overseen by multiple countries’ regulators. Though a regulator may seek to maintain market confidence, its regulatory turf is limited to domestic securities exchanges. For that reason, financial market authorities often seek to harmonize their restrictions across regulatory territories. In practice, this means that a domestic regulator must depend on a foreign regulator to extend the same ban. Otherwise, domestic securities listed abroad become vulnerable to the effects of short selling when short selling is not possible elsewhere.

For example, European countries coordinated short-selling bans during the stock market turbulence in March 2020. The national authorities in Italy, Belgium, Spain, and France issued one-day bans on the short selling of specific securities. Under EU Regulation No. 236/2012, Article 23, regulators who have observed price declines of at least 10% from the previous day are legally able to ban the short selling of the particular instruments for the following trading day. Article 26 requires the authorities to disclose to the European Securities and Markets Authority (ESMA) and other national authorities details about the intended measures (scope, duration, justification, and evidence) before imposing them. Article 26 permits other competent authorities, upon receiving the notification, to take supportive measures. For example, the United Kingdom’s Financial Conduct Authority (FCA) received notification of impending one-day bans from Italy and Spain on March 13, and from Italy, France, and Belgium on March 17. The FCA reciprocated the bans on the London Stock Exchange at the same time as the others. Similarly, the Bank of Ireland replicated the French one-day ban on Irish trading venues on March 17 without prohibiting the short sale of any Irish securities, and Germany took similar measures on its Tradegate Exchange, according to an ESMA Decision on March 16. Though none of the German, British, or Irish policymakers implemented broader short-selling bans on their domestic markets, they were able to assist the regulatory efforts of other European authorities.

Regulators worked through ESMA to take longer and broader actions. Under Article 27 of the EU Regulation No. 236/2012, ESMA has the power and responsibility to ensure that short-selling measures are consistent across competent authorities with respect to restriction type, scope, timing, and duration. ESMA arranged Austria, Belgium, France, Greece, and Spain’s short-selling ban commencements on March 17-18, renewals on April 15, and termination on May 18. Italy terminated its short-selling restrictions on the same day as the other countries—one month shy of Italy’s original end date, according to ESMA.

European regulators in non-participating countries addressed other bans in the bloc in March 2020. In the midst of Europe’s regulatory spate, the German regulator, BaFin, noted the European indexes that were exempt from restrictions. The Portugese Securities Market Commission (CMVM) did not prohibit short selling, but suggested it would keep the option open and expressed preference for short-selling intervention at the EU-level rather than the national level. Bulgaria’s Financial Supervision Commission signalled a similar message about its regulatory options, and explained that short sales were an “insignificant part” of Bulgarian financial markets and did not pose a threat to the country’s financial system.

Justification

Regulators observed both large price movements and uncertainty surrounding global health developments that threatened market confidence in implementing SSRs. Authorities acknowledged that these forces created market environments that were vulnerable to the effects of speculative short selling. They suggested that if short sales were left unchecked during a public health crisis, it could exacerbate ongoing market turbulence, create a crisis of confidence, damage the underlying companies, and compromise financial stability. Governments aimed to preserve market integrity by insulating their trading venues from the potentially negative effects of short-selling.

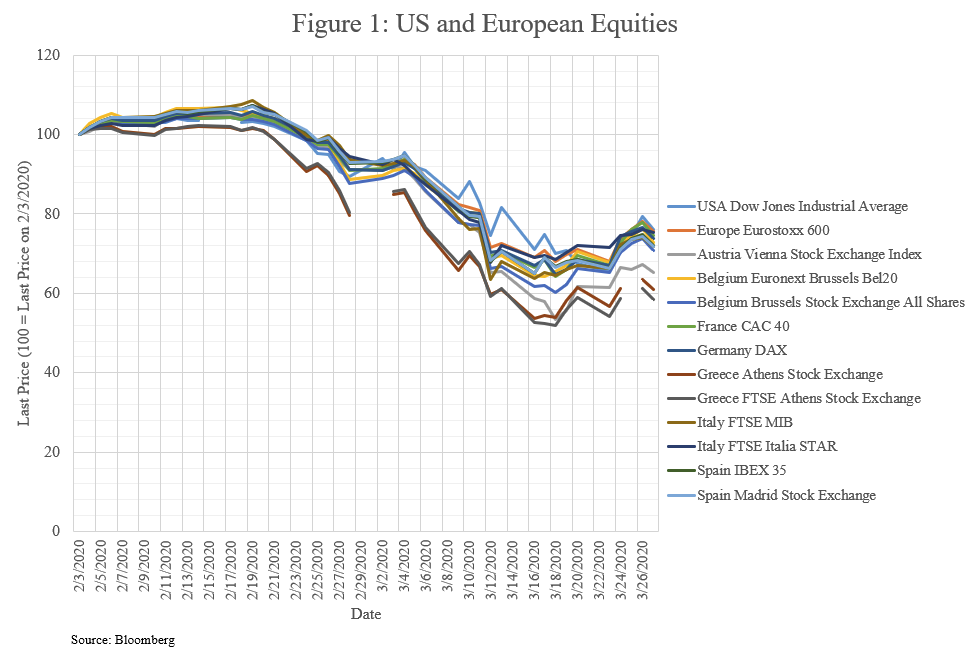

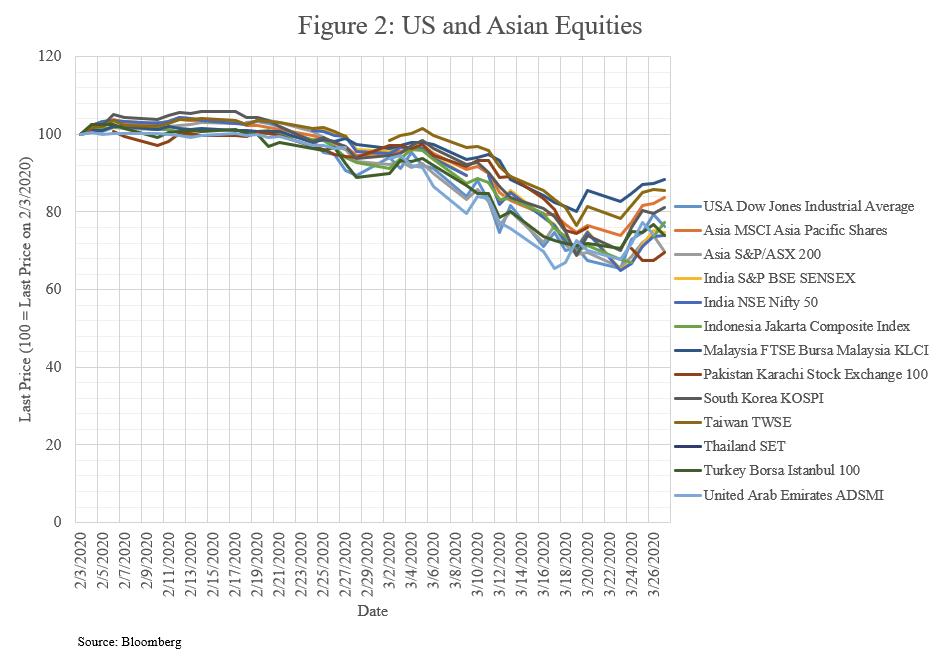

Late February to mid-March 2020 was a chaotic stretch for financial markets. The Dow Jones Industrial Average dropped 4.4% on February 27 (Tappe 2020). The next day, the German DAX fell 4.5% and the French CAC 40 index fell 4% (Smith 2020). Seven Asia-Pacific market measures, including South Korea’s KOSPI and Thailand’s SET composite index, also fell into correction territory on February 28 (Huang February 2020). After Pakistan’s benchmark index, the KSE-100, had triggered a circuit breaker on March 9, it ended the trading day at a 3% decline (Zubairi 2020). European stocks posted some of their worst one-day drops in history on March 12: the DAX was down 12.2%, the CAC 40 fell 12.3%, Italian stocks suffered single-day losses around 17%, and the pan-European Stoxx 600 index plunged 11% by the close (Smith and Ellyatt 2020). The Indonesian Stock Exchange halted trading for 30 minutes, after the JCI fell over 5% (Changole 2020). Thailand’s SET composite index plunged by 10% during the day, triggering a circuit breaker, and South Korea’s KOSPI index fell 7% (Huang March 2020). Malaysia’s FTSE Bursa Malaysia KLCI Index fell 4.42%. These trends are shown in Figures 1 and 2.

Of those that adjusted SSRs, most regulators spoke qualitatively about market turbulence. The South Korea’s Financial Services Commission (FSC) cited “market volatility amid concerns over a resurgence in COVID-19 cases” in August 2020, the Taiwan’s Financial Supervisory Commission (FSC) mentioned in May that “global financial conditions have recently triggered volatility” in securities markets, and Spain’s CNVM attributed March measures, in part, to “extreme volatility taking hold of European securities markets.” Authorities referred to prices from trading venues’ main and sector-specific indices. European regulators juxtaposed national volatility with global volatility, including the VIX (US) and VSTOXX (EU), in their comparisons. At least one Asian exchange, the Indonesian Stock Exchange, referred to month-over-month declines in the ASEAN countries’ most prominent indices (IDX 2020). The data spanned periods of time anywhere from a few days to over a month before the measures were implemented.

In addition to citing price movements, regulators described informational threats to market confidence: the uncertainty surrounding global health developments, an inability to price securities correctly, and constraints on supervisory and managerial duties. In March 2020, ESMA published opinions on the actions taken by several regulators, including Spain’s National Securities Market Commission (CNMV), Austria’s Financial Market Authority (FMA), and France’s Financial Markets Regulator (AMF). The opinions noted the spread of rumors and “false news,” through media outlets and social networks, about government decisions and the state of public health. They suggested this misinformation could negatively impact individual companies and investor confidence even during times of “efficient markets,” with publicly accessible and reliable information. However, during the COVID crisis, some authorities expressed their doubt that investors had “accurate and public information on the impact of the public health crisis on each listed company”—especially when large-scale health measures arrived suddenly and unexpectedly. They questioned the efficiency of markets during a pandemic, a time when “price formation may take place in an environment of partial information.” Multiple regulators claimed there was a disconnect between recent market movements and the underlying information that drove them. Austrian authorities referred to their policy measure as a “ban on speculative short-selling,” Belgian officials opined that “the market had difficulties correctly valuing the impact of COVID-19 crisis,” and the Italian regulator CONSOB claimed that the “information background [did] not fully validate the above-mentioned price fluctuation” (FMA 2020; FSMA 2020; CONSOB 2020). Finally, authorities noted that sudden lockdown and quarantine measures could hamper the critical functions of market infrastructures and supervisors, “putting both infrastructures and the supervisor at enormous strain to monitor, supervise, and manage markets.” Several European authorities suggested that issuers and financial market participants faced similar constraints on human resources. Regulators justified their SSRs because additional short-selling could exacerbate informational threats to market confidence, which could precipitate downward price spirals and increase systemic risk.

After recognizing the market-based and informational threats, regulators stated that the purpose of SSRs was to maintain market confidence. Indonesian authorities suggested that their market measures were meant to provide “legal certainty in facing the current circumstances” (OJK 2020). Belgian officials suggested that “the prohibition to open or increase net short positions would eliminate a factor that may play a significant role in exacerbating the fall of prices of shares admitted to trading on EU trading venues and therefore threaten financial stability” (FSMA March 2020). Malaysian authorities said that their ban was meant to “mitigate potential risks arising from heightened volatility and global uncertainties,” and referred to the intervention as a “short-term measure that sets to provide stability and confidence” (SC and Bursa Malaysia 2020). Regulators neither quantified market confidence nor described how it might be assessed or measured. Notably, no regulator cited theoretical academic evidence or past short-selling restrictions as evidence for the bans’ efficacy.

Restriction Type

“Covered” Short-Selling Restrictions

The most general short-selling limitation implemented in the wake of the COVID-19 pandemic prohibited transactions conducted with the intent of profiting from a decline in a given stock’s price. These general bans included both covered short sales, when a trader already secured the share or shares they intended to sell, and naked short sales, when the trader had not. All European regulators that banned shorting included such covered sales. None of the 17 countries that enacted new SSRs in 2020 had permanent bans on covered short sales of all stocks on their domestic exchanges and indices.

“Naked” Short-Selling Restrictions

Eleven of the 17 countries that implemented SSRs during the COVID-19 pandemic already had permanent bans on naked short-selling, heightening the chance of a failed trade. A trade fails (known as a failure-to-deliver, or FTD), when a buyer or seller fails to uphold the terms of a securities transaction by the settlement date (Bradford 2012). In the context of short-selling, a trade fails when the short-seller is unable to repurchase the shorted security from the open market and return it to the original lender. Scholarship exhibits a positive relationship between increased short-selling activity and the level of FTDs (Jain and Jain 2012). The individual consequences of FTDs can range from operational costs and fines to reputational damage (Sloan 2020). However, research also associates high levels of FTDs with high trading volumes more generally, which carry positive market effects, including reduced pricing errors, volatility, spreads, and order imbalances (Fotak et al. 2014). Though naked short-selling bans are proven to lower the level of FTDs overall, they also lower the market quality associated with higher levels of short sales (Jain and Jain 2015; Fotak et al. 2014). No new naked short-selling bans were implemented as part of broader financial stability measures in 2020. The Johannesburg Stock Exchange (JSE) Settlement Authority issued a market notice in March reminding its participants of its prohibition on naked short selling; however, the exchange did not broaden its restrictions during the crisis.

Net Short

Rather than prohibit short selling in its entirety, some regulators prohibited the creation or increase of net-short positions. Such prohibitions meant that market participants were able to short sell as long as they also took larger long positions on the same security. For example, Austria’s initial March 2020 ban applied to any short-selling transaction, but when the FMA extended the ban in mid-April, the regulator prohibited only actions causing net short positions. Belgium, France, Italy, and Spain followed a similar movement from covered bans to net-short bans. Only EU bloc countries and India enacted variations of net short-selling bans.

In addition to short selling, investors can also profit from a firm’s declining share price by using derivatives, such as buying put options. European policy makers stated in EU Regulation No. 236/2012 that the “calculation of short or long positions should take into account any form of economic interest which a natural or legal person has in relation to the issued share capital of a company or to the issued sovereign debt of a Member State or of the Union.” The calculation EU bloc authorities use if a regulator implements a net short-selling ban incorporates any benefits obtained directly or indirectly from derivatives such as options, futures, contracts for differences and spread bets relating to shares or sovereign debt, and indices, baskets of securities and exchange-traded funds. European policy makers stated significant sovereign debt net short positions could create systemic risk, and required national authorities to include credit default swaps relating to sovereign debt issuers when considering positions relating to sovereign debt.

The Securities and Exchange Board of India (SEBI) restricted exposure to index derivatives in March, stating short positions in these instruments could not exceed in value an investor’s holding of stocks held in cash. No other regulators limited index derivative holdings.

Scope

Index/Exchange-Wide

Financial regulators largely adopted broad bans, spanning the main indices, trading venues, and exchanges that comprised the home country’s capital markets. Twelve of the 17 countries that implemented SSRs during the COVID-19 pandemic prohibited short selling of any stock listed on indexes, trading venues, or exchanges. In its original March 2020 short-selling restriction announcement, the French regulator stated the new limitations applied when “the position involves a share admitted to trading on a trading venue in France and the share falls under the jurisdiction of the AMF within the meaning of the regulation.” The breadth of the bans reflected the pervasive effects of the COVID-19 outbreak across multiple markets and sectors within a given country, including systemically important institutions. In its corresponding March opinion, ESMA suggested that in lieu of broad bans, successive narrow restrictions, including sector or market-specific bans, might not have been as effective.

Several of the net-short bans also applied to instruments (including index-related instruments, exchange-traded instruments, or baskets of financial instruments) for which banned shares comprised a threshold proportion of the instrument’s weight. All of the European bans incorporated this condition; most regulators set their thresholds at a majority (at least 50%) of the instrument’s weight. On April 15, Belgium and Greece relaxed their relatively stringent thresholds from 20% to 50% of instrument weight, while Italy maintained 20% through the duration of its restriction. ESMA identified these related instruments as a part of each ban’s “strictly necessary scope,” yet the authority said it did not want to prohibit trading strategies that “provided an important service in terms of increasing liquidity and reducing volatility.”

Stock- and Sector-Specific

Several European authorities relied on short-selling regulations to protect specific stocks that experienced especially steep price declines. On March 12, Spanish regulator CNMV banned short sales of liquid shares admitted to Spanish stock exchanges whose price had fallen more than 10% and of illiquid shares whose price had fallen more than 20%. The regulator attached to its announcement a list of 69 companies that fit the description, which included travel firms and financial institutions, among others. Italian, French, and Belgian regulators made similar moves. Policymakers from the four countries eventually expanded the bans to their full stock exchanges.

Prior to the COVID-19 pandemic, the South Korean government enacted a rule that designates a stock as overheated if it meets certain performance thresholds, then temporarily bars investors from shorting it. South Korea’s FSC tightened these thresholds on March 10 to stem market volatility. A Korea Composite Stock Price Index (KOSPI) stock was labeled “overheated” if its price fell 5% or more compared to the previous day’s closing price and if its short-selling trading volume was three times higher than the normal average. The original volume limit was six times the average. A Korean Securities Dealers Automated Quotations (KOSDAQ) stock was considered overheated if its price fell 5% or more compared to the previous day’s closing price and had a short-selling trading volume of two times above the normal average. The limit was previously five times the average. The stock deemed overheated could not be shorted for 10 trading days, up from the one trading day required prior to the pandemic. FSC banned short selling entirely three days later.

No countries in YPFS’s survey enacted restrictions on short selling of shares in specific sectors, such as finance, during the COVID-19 pandemic. In contrast, most of the world’s leading stock exchange regulators used the finance-targeted approach during the Global Financial Crisis out of concern for financial institutions’ systemic risk. Thirteen countries, including various European nations, South Korea, and the US, banned the short selling of financial stocks, naked and not (Beber and Pagano, 2013; Beber et al., 2018). The U.S. Securities and Exchange Commission’s September 2008 ban included nearly 800 companies in the financial services industry, one of the most comprehensive and stringent. The regulator said it took the measure because there was an “essential link” between a financial company’s stock price and “confidence in the institution.” Then-SEC Chairman Christopher Cox said the sector-specific ban on short selling would “restore equilibrium to markets,” linking the financial services industry’s stock performance to broader market stability.

Exemptions

All of the EU bloc countries that implemented SSRs during the COVID-19 pandemic exempted actors performing market-making activities. A market maker, according to the U.S. SEC, “is a firm that stands ready to buy or sell a stock at publicly quoted prices.” Some researchers have argued that short-selling curbs make it difficult for market makers to provide liquidity (Jones 2012), which is all the more necessary in economic downturns. Greece’s March ban exempted market-making actions when the short-selling transactions were “conducted for hedging purposes.” Investors “hedge,” or offset potential losses, by taking the opposite position in the same security (or an index, option, or future that represents the same security). For example: an investor taking a long/buy position on security ABC might hedge against potential a decline in ABC’s share price by short-selling ABC at the same time.

In June, four months into its index-wide ban, Turkey exempted the top 30 shares in its sole exchange, Borsa İstanbul, from the short-selling ban.

Seller-Targeted

Turkey’s Istanbul Exchange attempted to block specific financial institutions from short selling on markets within its jurisdiction. Turkey in July announced that six international banks— Goldman Sachs Group Inc., JPMorgan Chase & Co., Merrill Lynch International, Barclays Bank Plc, Credit Suisse Group AG and Wood & Co.—were prohibited from short selling on the country’s stock market. Policymakers in other countries did not implement institution-targeted restrictions.

Timing and Duration

Sixteen of the 17 regulators that enacted SSRs during the COVID-19 pandemic implemented initial short-selling bans and restrictions in mid-March when governments began shuttering economies and markets began to decline in response. Turkey’s CMB was the first with an initial ban on short selling on February 28. Most European regulators that implemented restrictions initially reacted to volatile markets in mid-March by blocking short sales of particular stocks that had seen particularly sharp declines and later broadened their bans to entire indexes. Malaysia’s SC was the last to implement a short-selling ban, on March 23.

Many of the restrictions were extended while market conditions remained unstable. Most of the European bans were extended once and then collectively ended on May 18. Some regulators made their restrictions indefinite or extended them into 2021. In March, Turkey’s CMB said its short-selling ban would remain in place “until further notice,” the United Arab Emirates’ Securities and Commodities Authority (SCA) did not announce an end date for its prohibition, and on August 27, South Korea’s FSC extended its short-selling ban until March 2021.

Related Short-selling Rules

Transparency Requirements

Policymakers can also expand various reporting requirements for short sellers that are normally in place, such as EU authorities during the COVID-19 pandemic. Though it did not enact an EU-wide short-selling ban, ESMA in March 2020 lowered its short position reporting threshold, requiring holders of net short positions to notify the relevant EU regulating authority if the holding surpasses or meets 0.1% of the issued share capital of the company being shorted. The regular requirement previously kicked in at 0.2%. ESMA invoked Article 28 of EU Regulation No. 236/2012 to heighten reporting requirements in the EU. Requisite conditions must hold for the regulator to lawfully implement such an SSR, including addressing a threat to market integrity or financial stability in the bloc and taking an intervention measure the national authorities haven’t adequately implemented. When the requisite conditions are met, Article 28 also gives ESMA the power to implement broader SSRs, including a bloc-wide short-selling ban, but the regulator abstained.

Six other countries whose 2020 SSRs are described in this survey had variations of permanent short-selling transparency requirements prior to the COVID-19 pandemic. South Korea requires investors to disclose short-sale positions at or above 0.01% of a company’s outstanding listed shares. Short sellers in Thailand and Turkey have to mark their orders as such in the countries’ trading systems. Malaysia and Taiwan require investors to use specific systems to make short trades. Indonesia requires prospective short sellers to apply to make short trades on its exchange.

Managers of hedge funds, which contribute significantly to the practice, claim such disclosure requirements allow other investors to copy their short-selling strategies and thereby undermine them (McGavin 2010). Regulators claim reporting requirements allow them to police market manipulation, and the U.K.’s FSA has even argued that short-selling disclosure could “temper speculation and overreaction by investors to short-selling induced volatility” (McGavin 2010).

Uptick Rules

Regulators in three Asian countries, Taiwan, Thailand, and Pakistan enacted uptick rules. If a share on the Taiwan Stock Exchange declined 3.5% or more during the previous trading day, it could not be short sold below the previous day’s closing price—a measure adopted on March 20. The country originally had a 10% rule in place. In Thailand, short sellers could only execute trades when a share’s price was higher than its last quote, beginning March 13. Normally, the country mandates a share’s price be equal to or higher than the last trading price (known as a “zero-plus tick” regime) to conduct short sales.

The Securities and Exchange Commission of Pakistan (SECP) subjected 36 shares listed on its futures market to an uptick rule on March 18, targeting mostly energy and finance firms, such as Pakistan State Oil and the Bank of Punjab.

Volume Limits

Taiwan’s FSC implemented a curb on the total amount of short selling in which investors can participate. The policy, which took effect on March 19, limited the volume of short-sale trading orders to 10% of the average trading volume in any security over the last 30 days. This was down from an original 30%. It exempted certain market-making functions. The FSC was the only regulator YPFS has identified that used this strategy.

Settlement Procedure Changes

South Africa’s JSE Settlement Authority stated in March that it could force short sellers to borrow securities on the open market if it became aware that a market participant would not be able to settle a transaction. The regulator typically considers borrowing on behalf of investors who are short from 10 a.m. on the settlement date.

Related Policies

Regulators also enacted other policies in tandem with short-selling restrictions. In some countries, policymakers relaxed share buyback regulations in an attempt to support markets. Indonesia’s regulator announced in March that it would allow firms to buy back shares without prior approval in a general shareholders meeting. It also increased the maximum treasury stock resulting from the buyback to 20% from 10% from paid up capital. South Korea lifted stock buyback limits in March for certain qualifying companies.

Various circuit breaker changes were implemented in Asian countries in an attempt to stem market volatility, with regulators primarily lowering the drop percentage that would trigger an exchange closure. On March 17, policymakers in Thailand lowered the so-called “Level 1” circuit breaker trigger, the size of the drop on the exchange which halts trading for 30 minutes, to 8% from 10%. Thai regulators also tightened the Level 2 breaker and added a third.

Several countries closed their financial markets in response to the financial and health-related effects of the COVID-19 Crisis. The Jordan Securities Commission shut down the Amman Stock Exchange on March 17 to “protect Jordanian traders and companies from the great negative effects that the global financial markets are experiencing.” Similarly, the Kuwait Capital Markets Authority stopped trading on Boursa Kuwait from March 12 to 15 to combat “the fast-paced changes and turbulence facing the local exchange market, as well as regional and international exchanges, as a result of the COVID-19 outbreak” (Kamel 2020; Boursa Kuwait 2020). Sri Lanka’s Securities and Exchange Commission shuttered the country’s stock market from March 25 to May 11, holding that “under the prevailing conditions, the stock market will not be able to function in a fair, orderly and equitable manner.”

Though some authorities suspended financial activity with the aim of stemming market declines, several exchanges moved to remote trading for health reasons. On March 17 and 18, the Philippines Stock Exchange halted trading to comply with enhanced community quarantine guidelines, and moved to full offsite trading from March 19 to May 29. In the United States, the Chicago Board Options Exchange temporarily closed its options trading floor on Monday, March 16, and the New York Stock Exchange enacted similar measures one week later (CBOE 2020; Li 2020).

Evaluation

Analysis Conducted Pre-COVID-19

Scholarship asserts that covered short sales are generally beneficial to financial markets, though they can exacerbate the negative effects of market downturns. Subsequently, covered bans decrease the benefits of covered short sales, and push investors to rely on alternative strategies to establish short positions. Research also reveals that naked short sales have both market benefits and drawbacks, yet naked bans can cause overpricing and do not fully eliminate naked short sales and FTDs. Stock and sector-specific bans are generally regarded as ineffective.

Covered Short Selling

Research suggests short sellers can correctly predict price changes (Boehmer et al. 2008; Diether et al. 2009; Aitken et al. 1998) and are responsible for quicker movement of stock prices to their underlying value after a drop occurs (Lee 2016). Short sellers also appear to contribute to price discovery and efficiency by decreasing the prices of overvalued securities (Diether et al. 2009; Boehmer and Wu 2013).

Short-selling bans implemented during the wake of the GFC harmed market liquidity and slowed price discovery, according to a study by Beber and Pagano (2013). Boehmer et al. (2013) found a similar impact from the U.S.’s September 2008 ban. The U.K.’s September 2008 ban did not prevent financial stock price declines, though aimed to protect such stocks, and led to fewer price-forming trades (Marsh and Payne, 2012). Moreover, a study of short selling on the Hong Kong Stock Exchange suggested that short-selling does not cause irregular price movements during periods of heightened uncertainty (Crane et al. 2019).

Short sellers may shift their strategies to other instruments or markets, and evidence suggests the spillover can sometimes negatively impact the newly targeted market. Such sellers reroute their short positions to other venues where bans are not in effect, Shkilko et al. (2012) shows. As a result, liquidity shifts from regulated to over-the-counter (OTC) markets, according to Marsh and Payne (2012). Various studies have shown that the U.S.’s September 2008 ban resulted in inordinately higher spreads in the banned stocks’ option contracts (Battalio and Schultz 2011; Cakici et al. 2018; Grundy et al. 2012).

However, during periods of heightened market volatility, short sales contribute to downward price movements, but not as significantly as long sales, selling a security already owned, and there is no evidence that the short sales caused the initial downward movement, Shkilko et al. (2012) finds. Additionally, evidence suggests that shorting via high frequency trading (HFT) exacerbates illiquidity (Brogaard et al. 2017). However, the impact of short selling on price movements during calmer market periods is mixed. Short sellers could force down a given stock’s price by shorting in high volumes, a scheme known as a “bear raid,” but such stock manipulations are already prohibited by various statutes in most jurisdictions (Knowledge at Wharton 2008).

Naked Short-Selling

Research about naked short selling is limited because investors are not required to identify naked short sales, making them difficult to study. Researchers have argued that “both covered and naked short sales are generally transacted without actual prior or contemporaneous borrowing of shares,” and “the distinction between a covered and a naked short sale becomes functionally relevant only on the date of delivery when the naked short seller fails to deliver the security to the buyer” (Fotak et al. 2010). Researchers typically use FTDs as proxies for naked short sales.

Existing research about naked short selling’s impact on market quality is mixed. Lecce et al. (2008) used alist of Australian securities that were approved for naked short selling to study its effects. The practice causes a systematic increase in stock return volatility and deteriorates liquidity “via wider bid-ask spreads, decreased order depth and reduced trading volumes” (Lecce et al. 2008). The results of Culp and Heaton (2008) indicate that naked short selling may cause more volatility than covered short selling, largely because price drops take longer to recover from naked sales.

Fotak et al. (2010), however, studied a random sample of NYSE securities and found that an increase in naked short selling led to smaller pricing errors, lower pricing error volatility, reduced stock price volatility, and lower order imbalances. “The market impact of covered and naked short selling is very similar” (Fotak et al. 2010). Naked short sellers may be “contrarian investors who tend to target stocks following positive abnormal returns,” which is contrary, Boulton and Braga-Alves (2012) state, to arguments regulators make when curtailing the practice: naked short sellers intensify downward price movements.

Analysis of specific naked SSRs suggest such limits harm market quality. Particularly binding short sale constraints lead to extreme overpricing and subsequent reversion, according to Autore et al. (2015), a study of lists of excessive FTDs released by the U.S.’s three major exchanges. The authors use the SEC’s Regulation SHO as an example. The measure requires broker-dealers to close out failed short sales the day after the fail occurs. The Autore et al. (2015) findings suggest the SEC’s efforts to eliminate fails “could lead to greater overpricing as investors are forced to either borrow costly shares or forgo short selling stocks that are too costly to borrow.”

Two studies of the SEC’s 2008 ban on naked short sales of 19 financial stocks concluded that the prohibition adversely impacted various measures of market quality. The targeted stocks’ bid-ask spreads widened and trading volume decreased, according to Boulton and Braga-Alves (2010). Fotak et al. (2010) found “significantly higher absolute pricing errors and significantly lower trading volumes, indicating that the naked short selling ban hampered price discovery and reduced liquidity.”

Yet some evidence suggests that permanent bans on naked short selling do not fully stem the practice anyway. “The number of fails reported per quarter is an indication of the persistence of naked short selling, often in spite of regulations in place to bar” it (McGavin 2010). Stratman and Welbourn (2016) investigated stocks with high levels of FTDs, and the authors found that naked bans were not costly enough, or sufficiently “binding,” to deter informed investors from engaging in naked short sales. Rather, informed investors were willing to incur the regulatory penalties and high borrowing costs of illiquid stocks. Regulators in various jurisdictions have struggled to shore up legal tweaks to stamp out remaining naked short sales.

Stock- and Sector-Specific

Research also does not show that the narrow application of short-selling regulations to particular stocks or sectors is effective. The European Systemic Risk Board, responsible for EU financial stability oversight, found that short-selling bans attempting to protect institutions in the finance sector did not improve bank stability (Beber et al. 2018). In fact, their estimates, “even controlling for the endogeneity of the bans, point to the opposite result, namely that bans on short sales tend to be correlated with higher probability of default, greater return volatility and steeper stock price declines, particularly for banks” (Beber et al. 2018). It appears that short-selling regulations are ineffectual microprudential tools.

COVID-19

Preliminary research does not evaluate the effectiveness of COVID-era short-selling restrictions in achieving regulators’ goals, which they tended to define broadly in terms of market fairness, integrity, and confidence. Though supervisors attempted to maintain orderly and stable financial markets during the market upheaval, recent COVID regulations reinforced a scholarly consensus on the detrimental market effects associated with short-selling bans: market illiquidity, poor price performance, and increased informational asymmetries. The restrictions underwent political and corporate scrutiny before and after implementation.

It is a challenge to evaluate SSRs according to the authorities’ stated purposes because regulatory vocabulary is fluid (Austin 2017). Securities regulators that sometimes rely on a similar diction may actually follow different regulatory agendas. According to the International Organization of Securities Commissions, the objectives of securities regulation are to: (1.) protect investors; (2.) ensure that markets are fair, efficient, and transparent; and (3.) protect markets from systemic risk. Though COVID-era SSRs were often aimed towards achieving the second goal, the definitions of market fairness, integrity, and confidence are undefined--though often intertwined-- in national securities regulation. If there is no explicit definition for “market integrity” in a single country, it becomes challenging to understand how policy interventions--such as short-selling restrictions--might satisfy that definition. The advantage of this nonspecificity is regulatory flexibility, while the downsides include the uncertainty of regulatory progress and the possibility of overreach (Austin 2017). Additionally, conceptions of “market integrity” and related terms may differ from country to country, resulting in different regulatory practices once the terms are incorporated into law. One regulator might interpret “integrity” as a call to minimize market abuse and other illicit activity, while another authority might emphasize reliable price formation and equal access to information by market participants. The end result is that the regulatory success of SSRs could appear different from country to country. Overall, formal evaluations of SSRs appear to follow conceptual issues, and resist measurement along the regulator’s original language.

Emerging literature suggests that the COVID-era restrictions were similar to the GFC-era restrictions in terms of their effects on financial markets. Two recent studies investigated the effects of short-selling restrictions in six countries (Austria, Belgium, France, Greece, Italy, and Spain) and contrasted them with European counterparts that did not employ bans. Siciliano and Ventoruzzo (2020) observed higher informational asymmetries (via widened bid-ask spreads) and increased Amihud illiquidity (a ratio of stock returns to trading volume) in the ban countries compared to the non-ban countries during the SSR periods. The study shows that banned stocks underperformed comparable non-banned stocks, with average excess returns lower by about 0.1%. The negative effects were more pronounced with financial firms’ securities, an outcome that the authors attributed to the more widespread ownership of financial industry stocks.

Della Corte et al. (2020) also associated the COVID-19 bans with lower stock returns and increased illiquidity (via bid-ask spreads).

In a more narrow analysis, the Spanish market regulator CNMV observed the performance of stocks that were both banned on the Spanish Ibex 35 index and not banned on the German Dax 30 index (López and Pastor 2020). The authors found that banned stocks exhibited higher bid-ask spreads compared to their unbanned counterparts, yet the study could not attribute negative market consequences to the ban itself. The CNMV study demonstrates that individual European regulators did not achieve perfect coordination, though the alignment of restrictions was meant to prevent regulatory arbitrage.

All of the COVID-era studies acknowledged the issue of endogeneity, meaning that they were unable to conclude that the bans either caused or fixed market issues. However, the academic papers re-emphasized the ineffectiveness of short-selling restrictions and urged policymakers to reconsider instituting them during future market routs.

In a 2020 literature review of short-selling restrictions and stock exchange holidays, Luca Enriques and Marco Pagano claimed that market regulators and national competent authorities, by ignoring evidence and enacting the bans, had failed to learn the lessons of past mistakes. They quote former US SEC Chair Christopher Cox: “Knowing what we know now, I believe on balance the commission would not do it again. The costs (of the short-selling ban on financials) appear to outweigh the benefits.”

As authorities rolled out restrictions during the early stages of the COVID-19 pandemic, prominent policymakers and market representatives came out against the measures and cited a decade of evidence suggesting that these bans constituted poor policy. The former US SEC Chairman Jay Clayton resisted calls to ban short-selling, claiming, “You need to be able to be on the short side of the market in order to facilitate ordinary market trading” (Kiernan 2020). The World Federation of Exchanges, an industry group representing global stock exchanges with a collective capitalization of $95 trillion, warned regulators in March 2020 of the backwards effects of these market restrictions, and publicly asked policymakers to reconsider their positions in April and May of the same year.

In mid-2020, several media outlets accredited short sellers with the discovery of Wirecard’s massive accounting fraud, and some used the scandal to argue against recent SSRs (Bryant 2020; The Economist 2020). Wirecard is a large financial technology company headquartered in Ascheim, Germany. In 2019 a pair of Financial Times reporters raised doubts about Wirecard’s accounting practices, which caused volatility for the company’s listed shares and spurred German regulator BaFin to enact a short-selling ban of the company’s shares from February 18 to April 18, 2019 (Reuters 2019). A spokeswoman for BaFin, which did not implement broad SSRs during the COVID-19 pandemic, told media outlets earlier last year that the regulator did not plan to implement another ban on short selling of Wirecard shares (Reuters Staff 2020). The company later acknowledged in June 2020 that the company’s auditors were unable to find nearly $2.1 billion of its reported net cash, and admitted that the sum likely never existed (CNN 2020). After the company’s market value tanked and high-ranking executives were arrested on fraud charges, hedge fund representative Bryan Corbett wrote in the Financial News that short-sellers (of Wirecard) performed a public service by combatting the market desire to overprice a popular company. In light of the short-selling success, the author argued, regulators ought to have scrutinized corporate accounting practices rather than trading strategies. On November 3, 2020, ESMA released a Peer Review report that characterized the German financial supervisory treatment of Wirecard as “deficient.” ESMA claimed that the 2019 short-selling ban prompted a misunderstanding between German regulators, convincing another supervisor that BaFin “had no indications of wrongdoings by Wirecard” (ESMA 2020). The 2019 ban contributed to one of the many inter-regulator hiccups, which led to a lack of oversight on a fraudulent firm.

Despite the presence of strong anti-ban evidence and voices, some regulators still felt public pressure to take action to stem falling prices and heightened volatility at home, according to Bloomberg reporters (Weber and Brush 2020). In March 8 Tweet, Matteo Salvini, head of the Italian League Party, called for CONSOB to ban short-selling because “it is not tolerable for someone to take advantage of a national emergency by speculating to the detriment of Italian savings.” On March 17, French Minister of Finance Bruno Le Maire welcomed the AMF’s short-selling ban, and suggested the French government was willing to do whatever it took to keep French companies from going under, according to Reuters Staff. Short selling is a type of speculation on negative price movements, so the practice might become “politically unpalatable… or characterized as tainted by unethical goals” in the midst of a health crisis (Siciliano and Ventoruzzo 2020). Subsequently, short selling is ripe for prohibition during times of political and financial distress.