Cross-Margining and Financial Stability

This post comes to us from Joshua Younger, managing director for U.S. Fixed Income Strategy at J.P. Morgan. See here for the original article.

Over the past year, there has been considerable discussion of the market panic of 2020. Hindsight has provided an increasingly detailed view of what caused this episode, which not only saw extremely elevated levels of volatility across a variety of global markets but importantly near failures in their basic functioning. Nowhere is this more important than the market for U.S. Treasuries. Not only are they the risk-free benchmark that forms the foundation for roughly $50tn in U.S. fixed income assets, but since 2008 these securities have been imbued with cash-like characteristics. They are presumed to be monetizeable quickly, at low cost, and in functionally limitless size as woven into the fabric of macroprudential regulations.

In that sense, a breakdown in the functioning of the market threatens the stability of the system as a whole. Thus, it should come as no surprise that its near failure precipitated the largest intervention in the history of central banking. Over a roughly four-week period starting in mid-March of last year, the Federal Reserve (Fed) purchased nearly $1.7tn of Agency MBS and Treasury securities (~8% of 2019 U.S. nominal GDP) on a permanent basis, as well as offering overnight and term repo financing for another $6tn (nearly 30% of GDP), though only a fraction of that was actually used.

That this intervention was successful is no reason to sit tight—we of course cannot assume the Fed will come to the rescue next time. There is also arguably significant value to American taxpayers in ensuring Treasury securities continue to be relied upon, not just as a risk-free investment, but a store of value and source of liquidity. They should be a true and versatile safe haven.

Addressing these risks appears to be high on the agenda of policymakers. The Federal Reserve System has unsurprisingly focused on how its considerable firepower can be deployed to support the market (for example, here). More recently, Secretary Yellen highlighted the systemic importance of the Treasury market at her inaugural Financial Stability Oversight Council Meeting, and Undersecretary-designate Liang considers it a key focus of her tenure[1]. The most recent meeting of the Treasury Borrowing Advisory Committee (TBAC) meeting included a lengthy discussion of several troubling events, including the COVID-19 panic. The same document explores several proposed measures to address vulnerabilities in the Treasury market, many of which—like central clearing of the Treasury market, closer supervision of non-bank intermediaries like hedge funds, etc.—have been broadly discussed in various forms. One suggestion that has received comparatively less focus, but arguably has the most immediate potential to address these issues, is reconsidering margin requirements on a variety of levered transactions.

Margin is set to offset counterparty risk in levered transactions. In most cases, there are two such requirements: first, variation margin (VM), in which collateral is posted by the party taking losses to protect the unrealized gains of the other, and second, initial or maintenance margin (IM), which provides additional protection (overcollateralization) against the practical uncertainties of dealing with defaults and liquidations. They are generally set either by centralized clearing counterparties (CCPs), where applicable (e.g., the listed futures market and most OTC swaps), or are negotiated on a bilateral basis (e.g., repurchase agreements and swaps not subject to mandatory clearing). Maintenance margin, in particular, is often a key driver of overall leverage capacity in the financial system, particularly in futures and other derivatives markets. It is also inherently pro-cyclical: when volatility is elevated, so too are the risks associated with the sale of collateral to cover liquidated positions, leading to commensurately higher maintenance margin requirements. This can drive further increases in volatility as levered investors sell assets to raise the cash to meet these margin calls—a potentially vicious cycle.

Due to practical and legal constraints, margin requirements are mostly set by the CCPs on the basis of their own risk rather than the economic exposure of market participants. As a result, portfolios that are preferentially long one type of instrument—for example, Treasury securities—and hedged with another—short futures on the same—will have to be treated as separate, outright exposures. That means that when volatility picks up, even if the portfolio is nearly perfectly hedged and exhibits virtually no change in value, the aggregate margin required to maintain those positions can increase dramatically. If for any reason those calls cannot be met on any component of the portfolio, they can be subject to forced sales and liquidation.

With the possible exception of 2008, at no time was this risk greater than in the spring of 2020. The spike in volatility led to significant margin calls across global markets. Though more realistic portfolios are more complicated; for example, the maintenance margin on various futures contracts increased substantially over this period—in many cases by a much larger amount than was true around peak of volatility in 2008 (Exhibit 1 & 2). We can see the impact most clearly in cash deposited at the Fed by financial market utilities, which includes the most systemically important CCPs, and increased sharply—more than $200bn over two weeks in March 2020, the largest such monthly collection since data became available. More granular disclosure[2] shows a more than $230bn IM call across major U.S. and European CCPs, but the bulk came from futures and options cleared through the CME. Their disclosure also shows that maintenance margin requirements, rather than variation margin, drove these calls[3], suggesting that the primary driver was increased risk aversion among CCPs rather than rapidly accumulated losses on existing positions (Exhibit 3 & 4).

Setting margin requirements based on their own exposure is simply prudent risk management on the part of CCPs and others. Unfortunately, conservative decision making at the microprudential level may not necessarily fit well with macroprudential risk management. In this case, the risk was that these calls would force the liquidation of relative value positions, particularly Treasury securities held against futures contracts (basis positions) that were otherwise reasonably well-hedged with theoretically bounded terminal outcomes. Whether or not those unwinds occurred, markets quickly priced in significantly increased risk of such an outcome.

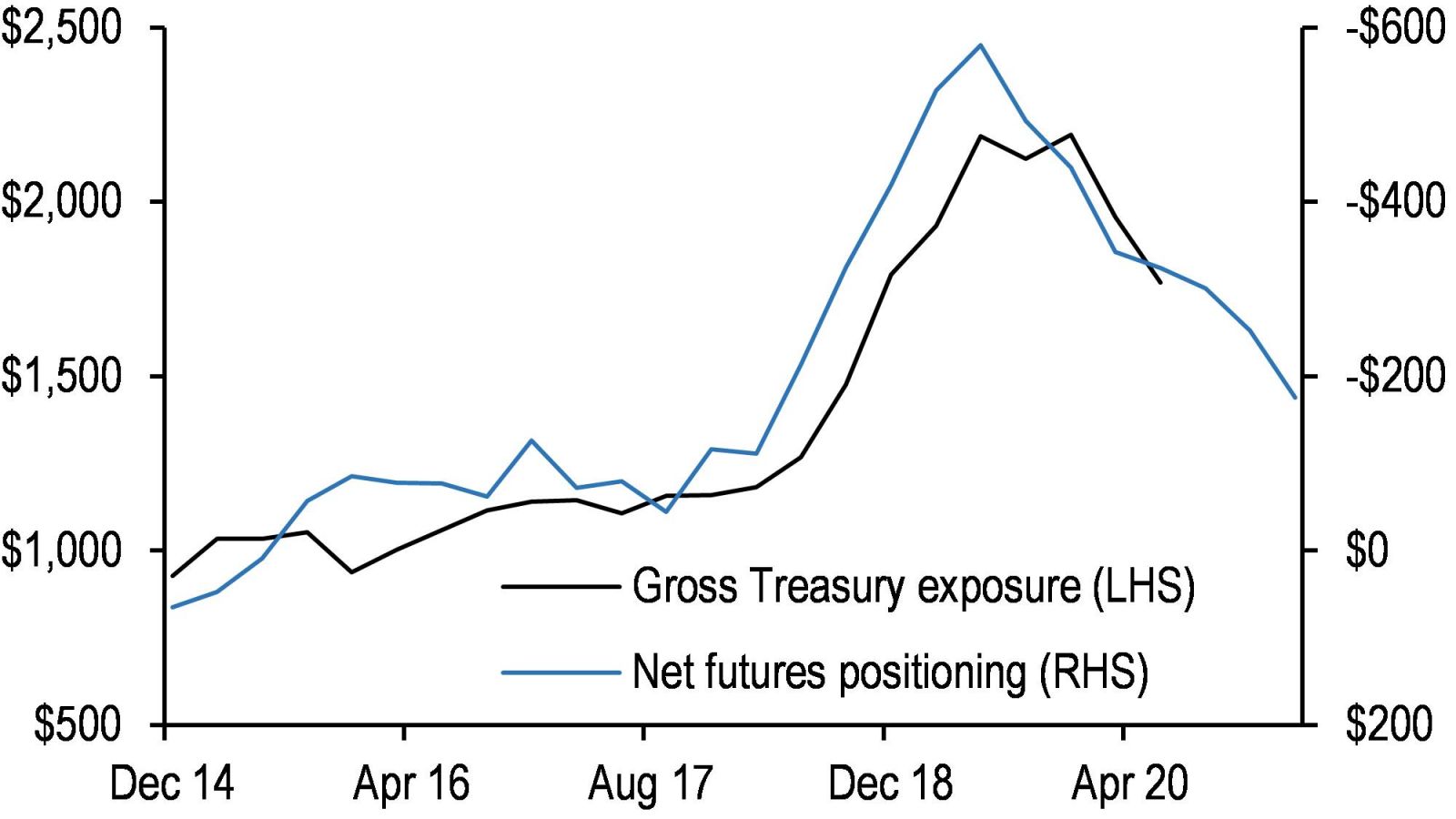

These exposures were large—likely in excess of $200-300bn notional—but more importantly served a critical link in market functioning. Highly levered positions, mostly held by hedge funds and other more speculative market participants, constituted a kind of shadow dealer network for Treasury securities. How they took on this role has been examined in detail elsewhere but is reflected in the sheer quantity of Treasury collateral locked in the hedge fund complex: more than $2.2tn of 4Q 2020, nearly doubling over just a couple of years and associated with a similar build-up of a large net short in Treasury futures (Exhibit 5). As a general matter, this looks quite a bit like a traditional market maker portfolio, in which inventories of off-the-run securities are hedged with a mix of shorts in futures and more liquid current issues. Though SEC data on cash exposures is only updated through 3Q 2020 owing to reporting lags, it shows initial evidence of a rapid reduction in this position, which futures data suggest has continued but is not yet wholly unwound. In that sense, shadow dealing likely remains a key component of Treasury market structure.

Margin calls may not have explicitly triggered liquidations and forced sales. But markets operate and price risk according to the perceived range of plausible outcomes. As a critical link in the secondary market, even a somewhat more probable outcome had the potential to change perceptions of liquidity risk in the market more generally. In practice, this led to higher transaction costs. Bank-affiliated dealers grew increasingly balance sheet constrained and were forced to price market making so as to discourage taking on new positions faster than they could be recycled by the market. The increased likelihood of margin calls leading to forced sales—imagined even if not imminent—most likely played a role in generating and exacerbating market dysfunction.

What is the solution? We are all arguably better served by margin requirements sized to the market risk of participants, rather than the individual exposures of each CCP[4]. So-called cross-margining involves setting up the information technology and legal infrastructure to allow loss sharing between two (or more) CCPs in the event of a default or liquidation. Doing so generally leads to lower maintenance requirements on well-hedged positions like cash/futures basis trades. It would also allow minimums to be set more conservatively relative to market risk, making it much less likely that they would have to be raised quickly in the event of a volatility shock like last March and April. Reducing the risk of liquidity shocks triggered by liquidations of otherwise well-hedged and low-risk positions is at the core of good macro-prudential policymaking.

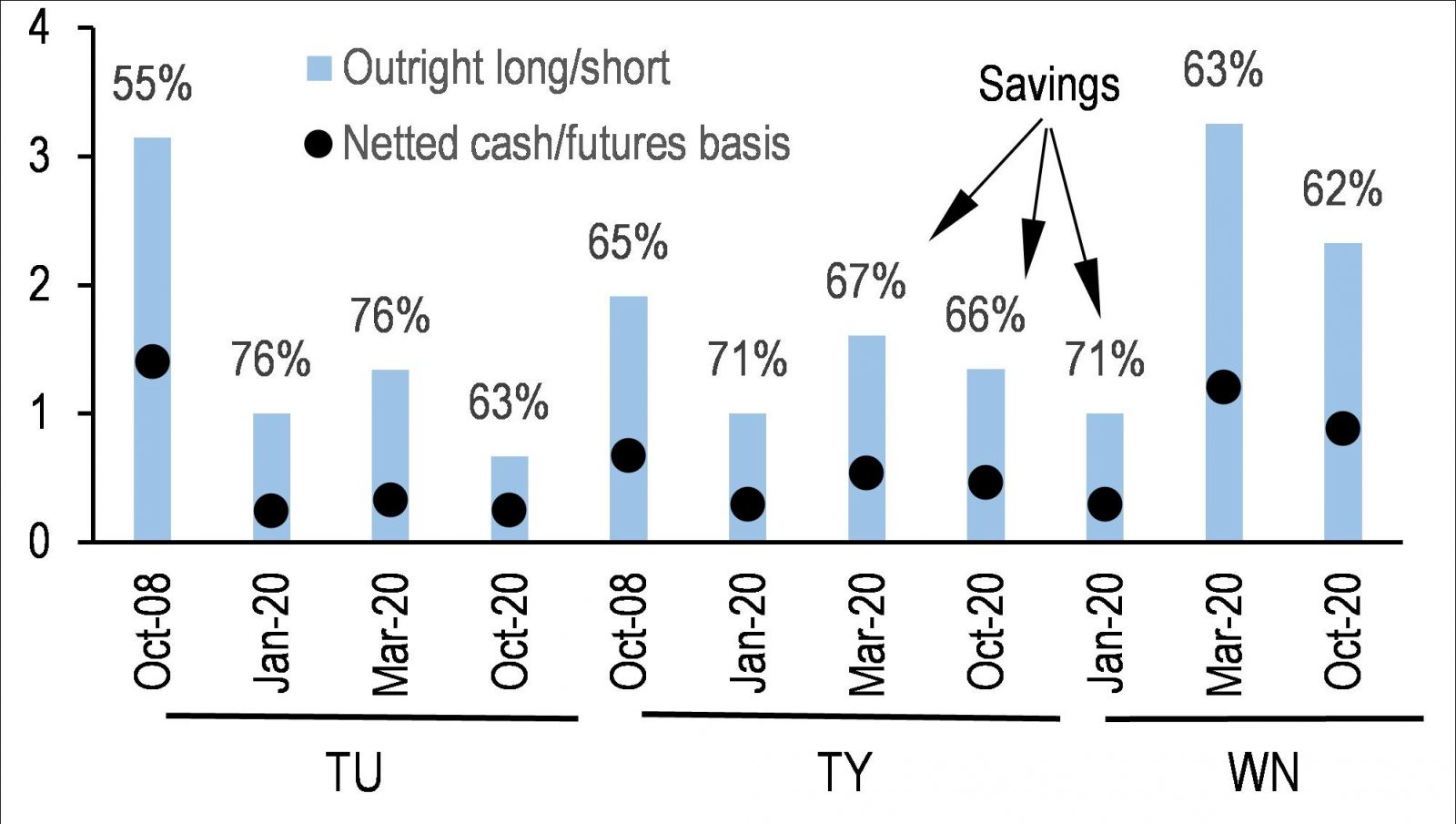

To get a more quantitative sense of how IM requirements would change if they incorporated risk offsets from cash and futures positions, we consider longs in CTD cash/futures basis across a range of contracts for evaluation dates in the fall of 2008 (for TU and TY) as well as January versus late-March 2020 (Exhibit 6). The results show a significant savings—often more than 70%. This would, of course, allow for more leverage in the system, all else equal, which is not necessarily desirable. That said, even the peak IM with risk offsets is comparable to outright requirements before the COVID shock. That suggests CCPs could adopt very conservative levels relative to economic risk but comparable to current minimums while also significantly reducing the risk of needing to raise them meaningfully under stress. In that sense, more broadly available cross-margining of cash and futures positions could allow for higher levels of effective overcollateralization in basis positions as well as less variability in those requirements under a very wide range of market environments.

Doing so would make for good microprudential policy as well. That CCPs currently set their margin requirements based on their own exposure is both understandable and prudent. But doing so has the potential to create new vulnerabilities. In 1987, for example, separate margin calls for equity options portfolios and the futures positions used to hedge exposure to the underlying arguably contributed to the near-failure of some CCPs on “Black Monday.” The introduction of cross-margining was high of the list of reforms proposed by several groups (e.g., here, here, and here) to improve market stability, which led directly to the introduction of cross-margining agreements between the Options Clearing Corporation (OCC) and Chicago Mercantile Exchange (CME). More recently, the CFTC ran stress tests across a wide range of CCPs in late-2016 and found many FCMs who faced significant losses on one were managing gains on the other, which suggests that these gains could be used to offset losses under stress, strengthening the risk position of the CCPs individually as well.

That is not to say broadly available cross-margining of cash and futures positions in Treasury securities would have prevented the market dysfunction of March 2020, nor would it necessarily do so in the future. Other reforms can and should be implemented, in our view. But this is arguably low-hanging fruit. Not only have such arrangements been implemented in the past, but the CME and Depository Trust Clearing Corporation (DTCC)—which clears a significant fraction of Treasury securities owned via repurchase agreements—have a preexisting relationship and are already looking into ways to expand its reach. Legal and logistical hurdles definitely remain[5]. And of course it becomes substantially more effective if paired with a clearing mandate for the Treasury market, as some have proposed. But the process of implementing reforms to improve the stability of the Treasury market under stress, expanding cross-margining and reducing the risk of pro-cyclical margin calls is likely an attractive plank.

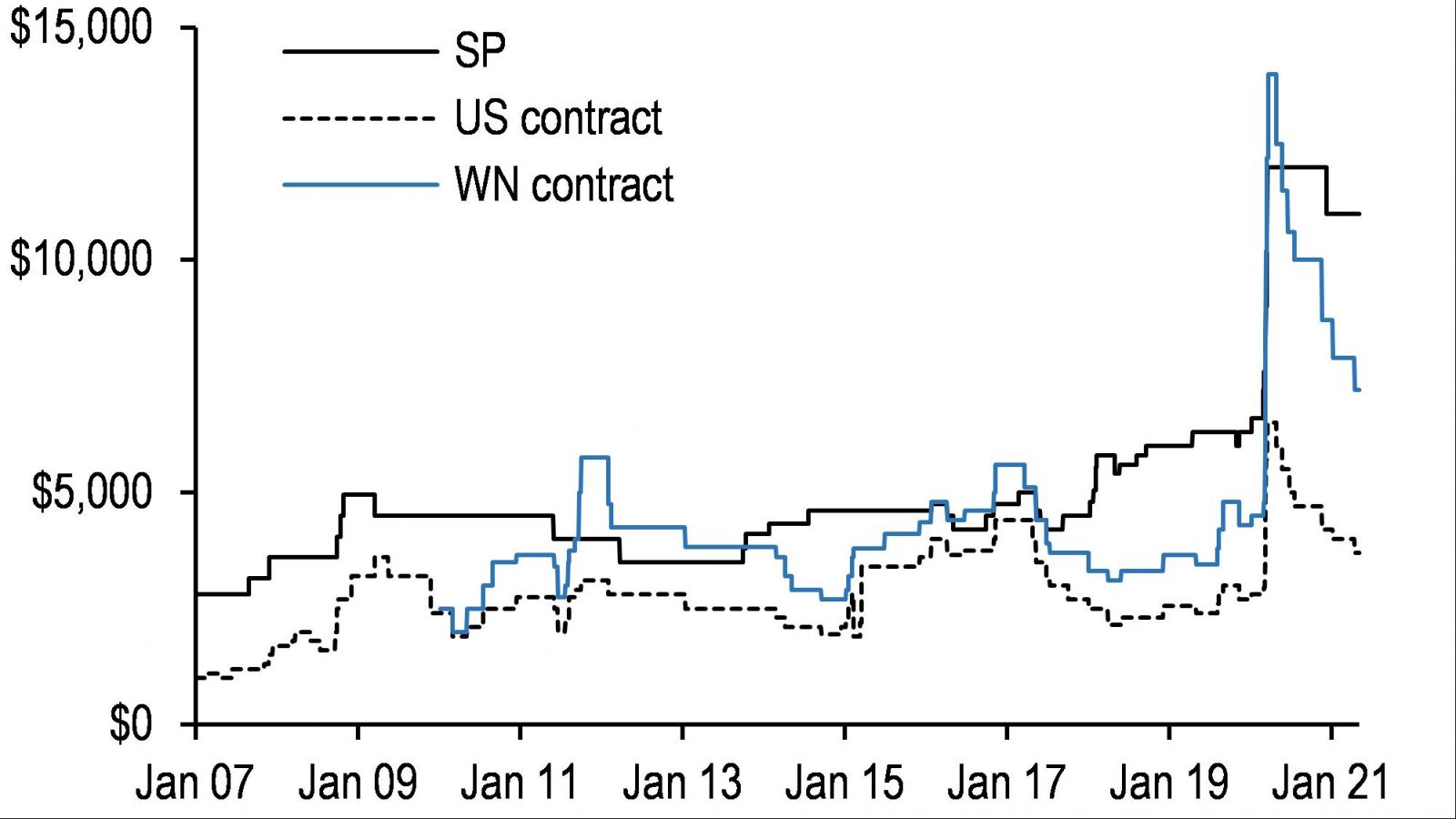

Exhibit 1: Maintenance margin requirements increased sharply in March 2020 as CCPs raced to protect themselves against rapidly increasing volatility …

Maintenance margin for outright longs in SPX, US, and WN futures; $ per contract

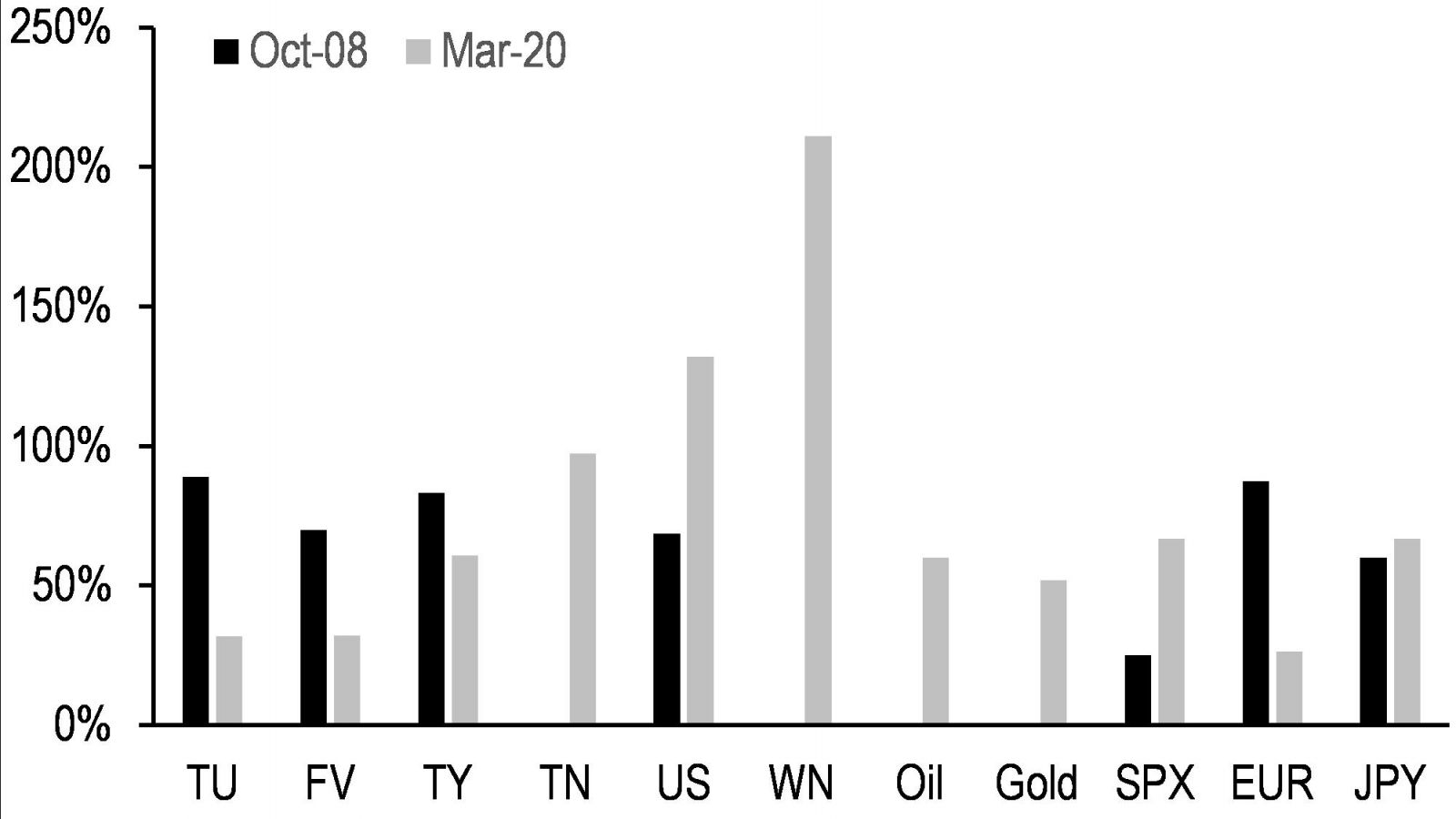

Exhibit 2: … which, in many cases, resulted in relative margin increases that were comparable to if not larger—in some cases much larger—than

the fall of 2008

1-month change in maintenance margin for outright positions in various futures contracts; %

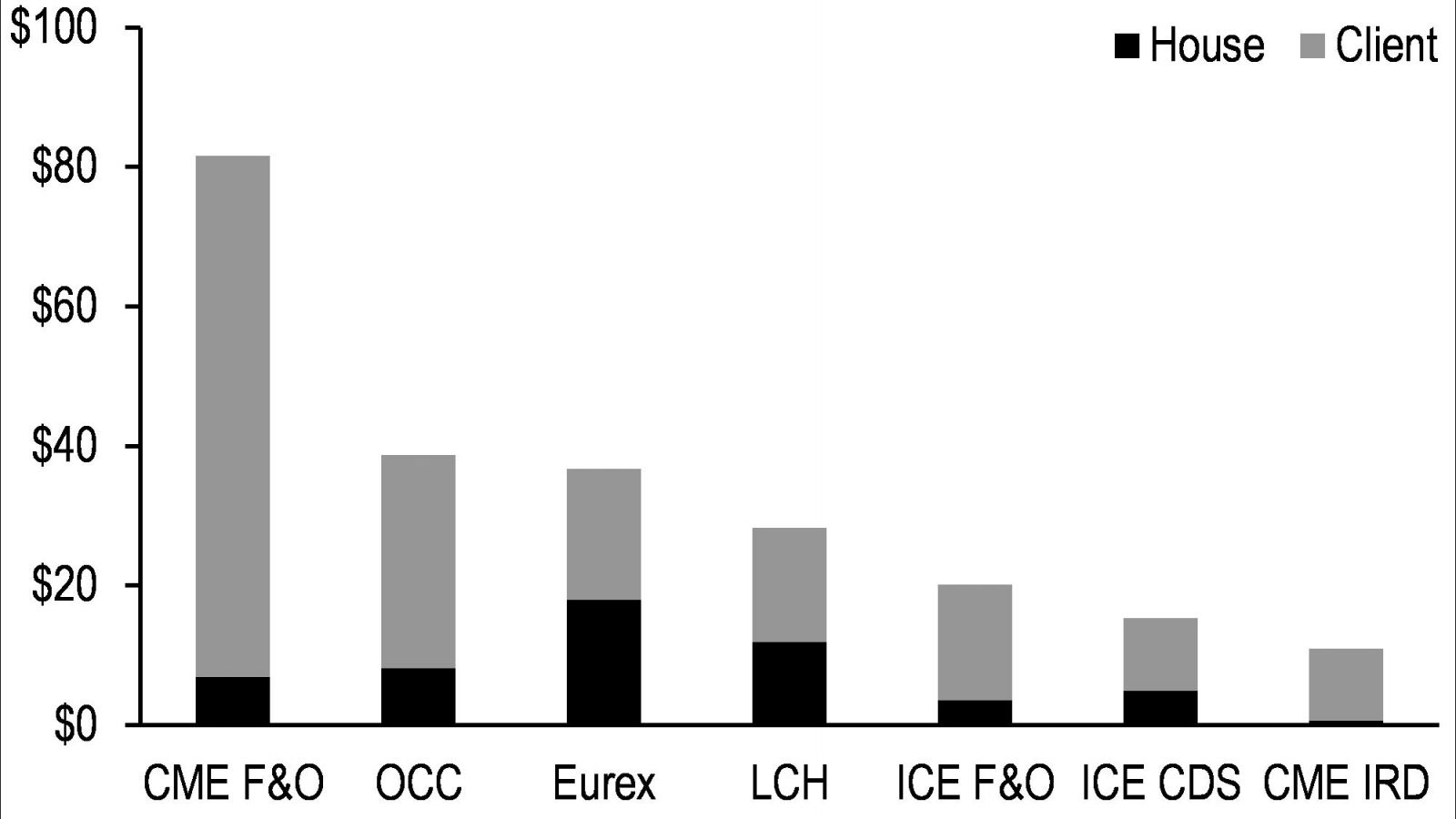

Exhibit 3: The largest CCPs collected more than $230bn in initial margin over 1Q 2020 across asset classes, the bulk of which were related to CME-listed futures ...

Change in initial margin held by each CCP from 4Q19 to 1Q20 split into house and client accounts by clearinghouse; $bn

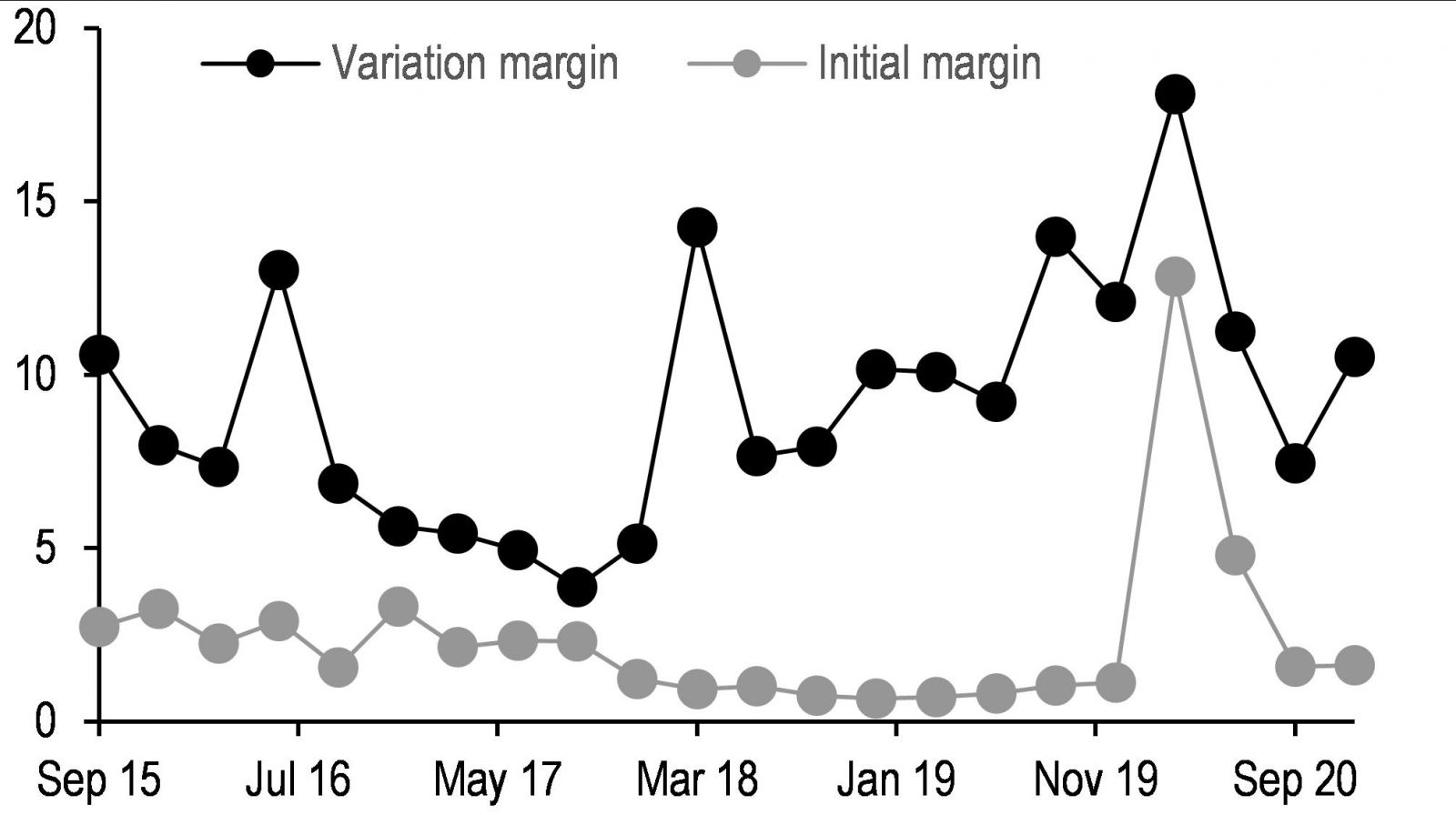

Exhibit 4: … and for CME specifically initial margin calls were much larger relative to their history than variation margin

Largest daily IM and VM calls related to futures and IRS cleared through CME by quarter; $bn

Exhibit 5: The rapid growth in gross exposure to Treasury securities among hedge funds came with a similar build-up in net short futures, both of which have been substantially but not wholly unwound

Gross exposure to Treasury securities among hedge funds tracked by SEC Private Funds Statistics (data through 3Q20; LHS) and net futures positioning among levered funds from CFTC reporting (inverted, as of quarter-end; RHS); both axes in $bn

Exhibit 6: Allowing cross-margining of cash/futures basis positions would significantly reduce IM requirements and could allow for more stable and conservative minimums

IM requirements of outright and netted CTD cash/futures basis positions by evaluation date, both normalized to 1.0 for outright positions as of January 2020, with savings indicated above; unitless

[1] See also Enhancing the liquidity of the U.S. Treasury Market under stress, N. Liang & P. Parkinson, Brookings (December 2020)

[2] Standardized CPMI-IOSCO Quantitative Disclosures were specified in 2012 and have continued quarterly, though often with a significant lag. The most recent data are as of Q4 2020.

[3] Though the maximum total variation margin call in 1Q 2020 was optically larger, it was also not particularly inconsistent with much lower volatility environments. The largest total initial margin call, by contrast, was significantly larger than any prior period covered by these disclosures.

[4] A related but somewhat different consideration is a congruence principle for macroprudential regulations, discussed in detail by Metrick & Tarullo (2021).

[5] Direct FICC membership remains largely limited to dealers and banks. Sponsored member has of course taken on an increasing share of the volume—typically $200-300bn per day, and higher around statement dates like year-end—which in principle means a significant fraction of turnover in repo markets is eligible for cross-margining against futures positions. However, some implementations could run into regulations requiring strict segregation of client and house funds, which treat FCM and sponsored margin differently.